1. Problem

The question was simple and uncomfortable: was a 30 percent collateral floor actually enough to protect the rewards system under realistic volatility? The answer mattered because intuition around safety margins is cheap and tail events are not.

2. Approach

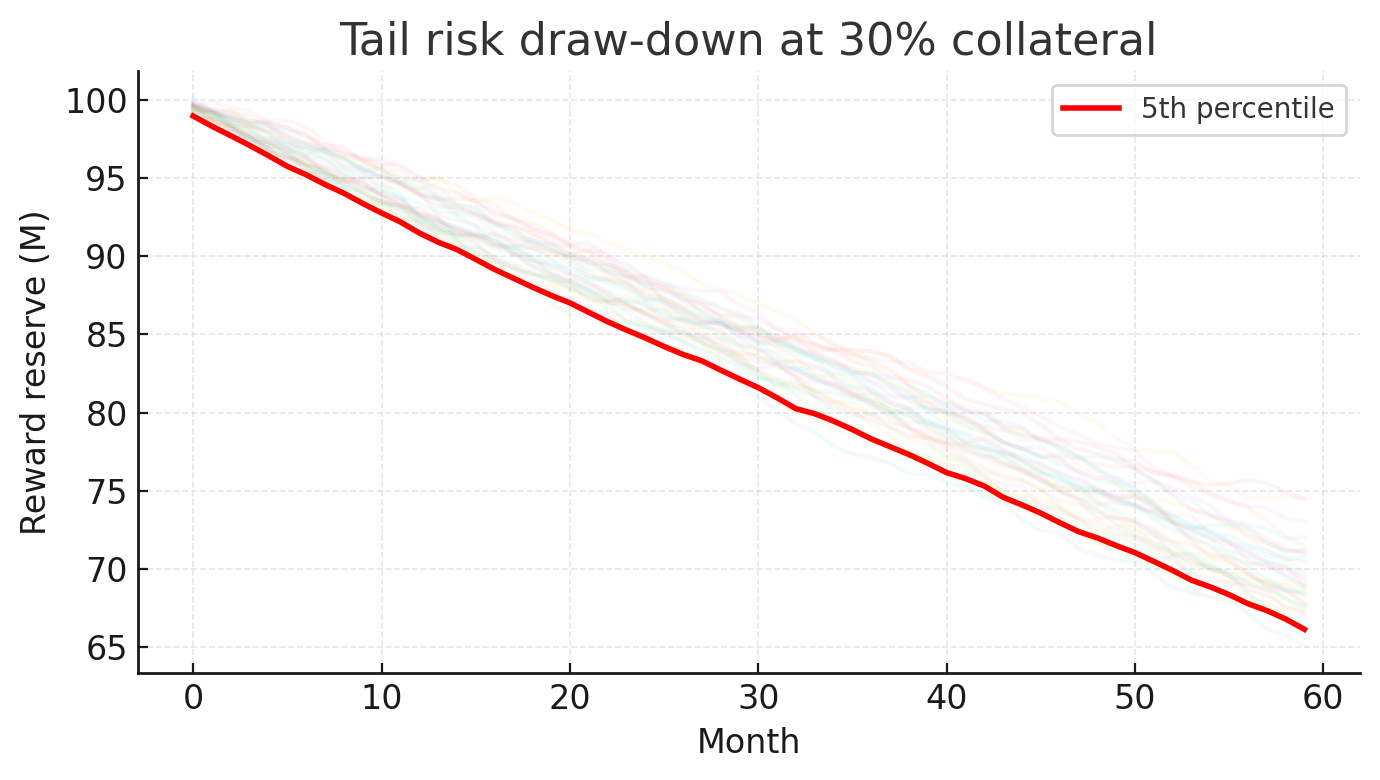

I built a Monte Carlo stress test that linked price volatility, capacity growth, utilization, and reserve depletion. The point was not to produce one magical number. It was to map how insolvency risk behaved under different collateral floors.

- Simulate thousands of price paths over a multi-year horizon.

- Model reserve drawdown when utilization weakens.

- Compare insolvency probability at different collateral thresholds.

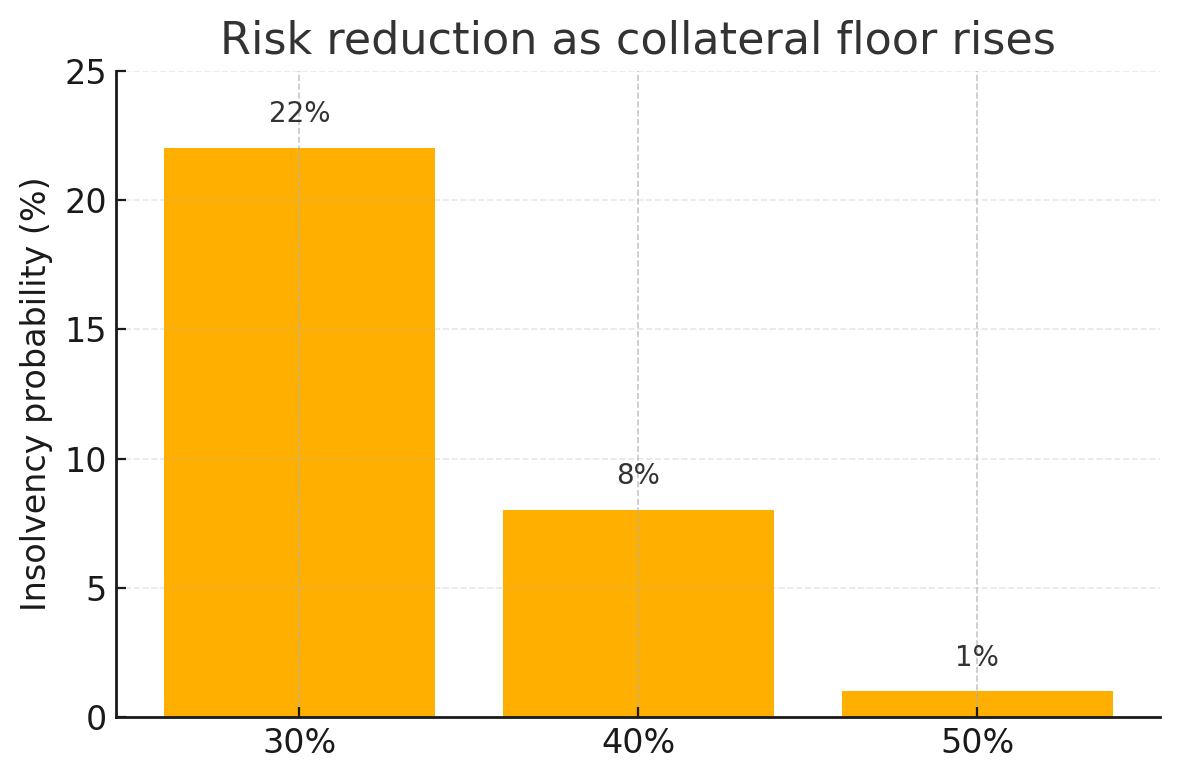

3. Evidence

4. Outcome

The modeling supported a move to a 50 percent collateral floor, cutting modeled insolvency risk sharply and giving governance and engineering a much clearer rationale for the change.

5. Tech stack

- Python with NumPy and Pandas for the simulation engine

- Matplotlib for scenario visualizations

- Integration with on-chain design and downstream monitoring

6. Useful links

7. Related reading

8. Call to action

If you need to turn a vague risk debate into a model with decision-grade outputs, I can help design the simulation and the narrative around it.